What Is Bitcoin? The Digital Currency Challenging Gold and Central Banks

Bitcoin is often described as digital gold. The label is useful, but it is still too small. When the pseudonymous Satoshi Nakamoto published the Bitcoin white paper in 2008 and launched the network in 2009, the goal was not simply to create another tradeable asset. It was to build money for a digital world, where value can be stored, moved, and verified without asking an institution for permission.

That matters because Satoshi is not presented here as a founder in the corporate sense. He is the pseudonymous author of the white paper and the original architect of the protocol, but Bitcoin was designed so that the system would not depend on his continued presence. That absence is part of the point.

That is what makes the comparison with gold and central banks so important. Gold helps explain why scarcity matters. Central banks help explain why control over money matters. Bitcoin sits between the two, and in some ways against both of them.

The point of this article is not to argue that Bitcoin has already replaced the old system. It has not. The more useful question is simpler: what problem was Bitcoin built to solve, why does that problem still exist, and why does Bitcoin matter even when most users first meet it through ETFs, exchanges, or custodial apps?

What Is Bitcoin?

Bitcoin is a monetary network built to let people hold and transfer value without asking permission from a bank or a central authority. It is open source, globally accessible, and designed so that anyone can verify the rules for themselves.

That is the part that tends to get lost when Bitcoin is reduced to a price chart, an ETF ticker, or a speculative trade. Bitcoin is not just an asset. It is also a protocol, a network, and a monetary rule set. If you strip away the market noise, what remains is a simple but unusual idea: money can be governed by software, and the software can be open enough for anyone to inspect it.

At a practical level, Bitcoin does three things at once. It lets users send value directly to one another. It makes the supply rule public and predictable. And it allows anyone to check that the system is following its own rules.

That last point matters more than it first appears. In traditional money, most people do not verify anything themselves. They trust banks, payment processors, central banks, and the institutions around them. In Bitcoin, the goal was different from the start. The rules are supposed to be visible, auditable, and hard to change.

Bitcoin is often compared with gold because both are scarce, both can serve as stores of value, and both sit somewhat outside the discretionary control of a central issuer. The comparison is useful, but it also misses the main difference. Gold is a physical asset that needs custody. Bitcoin is native to the internet. It can be moved across borders, checked by software, and held without a vault, a shipping network, or a custodian.

That design choice, from Satoshi’s original proposal, is what makes Bitcoin feel less like a financial product and more like a monetary protocol.

Bitcoin is also not “just a blockchain.” The blockchain is only one piece of the architecture. What makes Bitcoin work is the combination of distributed nodes, proof of work, consensus rules, cryptographic ownership, and a fixed issuance schedule.

So the short version is this: Bitcoin is a system for turning trust into verification. That is its real innovation, and it is also why it is more than just a tradeable asset.

What Problem Does Bitcoin Solve?

To understand Bitcoin, it helps to start with the problem it is trying to solve.

The modern monetary system works because people trust institutions. We trust banks to hold deposits. We trust payment providers to move funds. We trust central banks to manage the currency. We trust states to maintain the legal framework. That trust is useful, but it also creates fragility, because it means the user rarely controls the asset directly.

🪙 Is Bitcoin (BTC) Really a Currency?

If your money sits in a custodial account, you do not fully hold it in the same way you would hold cash in your hand. Access can be delayed, restricted, frozen, surveilled, or conditioned. That is not necessarily because something has gone wrong. It is simply how the system is built.

Bitcoin was designed as an answer to that dependency, and the answer is broader than the usual “peer-to-peer money” slogan.

Money based on trust creates structural risk

In a fiat system, the final unit of account is issued by a central authority. That means the supply of money can expand, contract, or be redirected through policy. It also means ordinary users do not have direct control over the asset they are using every day.

The practical result is not always dramatic inflation. More often, it is a slow erosion of purchasing power that becomes visible only over time. That changes behavior. Households move into real estate, equities, credit, or other assets just to preserve value. In that sense, the system pushes people to become investors whether they wanted that role or not.

Bitcoin starts from a different premise. Instead of assuming that monetary supply should be managed by discretion, it encodes a supply rule into software and makes that rule visible to everyone.

Intermediaries create convenience, but also vulnerability

Banks and platforms are useful. They make payments easier, and for many users that convenience is worth the trade-off. But the trade-off is real, and it becomes obvious the moment an intermediary fails, freezes an account, or changes the rules.

Intermediaries can fail. They can be hacked. They can mismanage reserves. They can impose restrictions. They can also become political pressure points.

Bitcoin does not eliminate all risk. It changes where the risk sits. Instead of relying on a third party to be honest forever, the user can, in principle, hold the asset directly and verify the system independently. That is a major shift.

Money is also political

Monetary policy is not neutral. When a central bank changes rates, expands liquidity, or supports financial institutions, the effects are distributed unevenly. Some actors benefit earlier than others. Some asset prices react before consumer prices do. Some forms of savings are protected, others are diluted.

Bitcoin removes monetary issuance from discretionary control. It does not guarantee a better policy. It guarantees a different rule.

The digital age makes the problem sharper

In a physical cash economy, using money without intermediaries was easier. In a digital economy, money is increasingly mediated, tracked, and programmable. The more financial life moves online, the more control becomes centralized.

That is the deeper context for Bitcoin. It is not only about protecting against inflation. It is also about preserving a form of monetary independence in an environment where money is becoming more surveilled and more dependent on software owned by someone else.

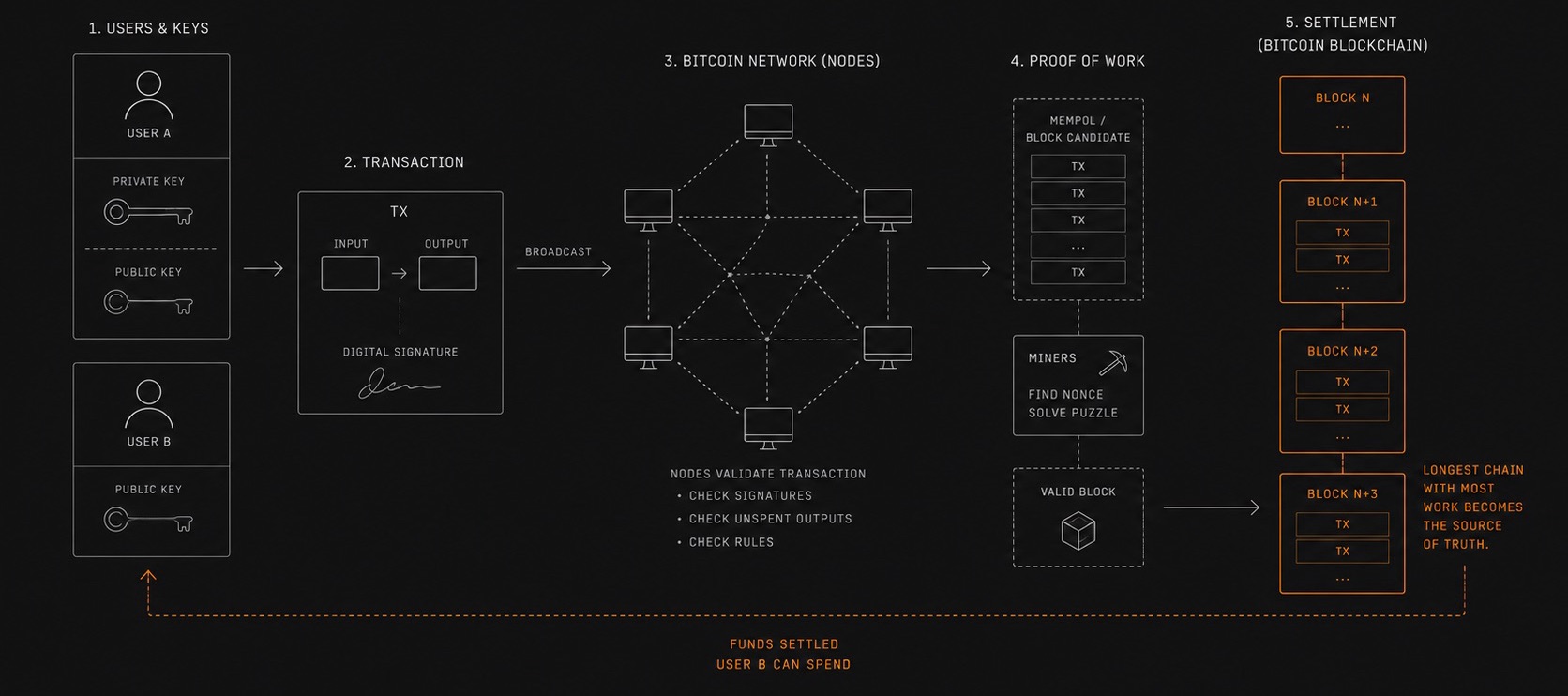

How Does Bitcoin Work?

Bitcoin works through a combination of network rules, cryptography, and incentives.

At the center of the system is a peer-to-peer network. There is no central server deciding which transactions count. Instead, nodes run software that checks the rules independently. If a block or transaction violates those rules, honest nodes reject it.

That is one of Bitcoin’s most important properties: users do not have to ask permission to verify the system. A node does not need to trust a bank, a payment processor, or even a miner. It only needs to check whether the transaction follows the protocol rules.

A network of rules, not a company

This distinction is easy to miss, because many users first encounter Bitcoin through exchanges or apps that look like ordinary fintech products. But those interfaces are not Bitcoin itself. They are only access points.

The network is something else. It is a set of rules that define how value moves, how new coins are issued, and how the ledger is updated. Remove the company layer, and Bitcoin still exists. Remove the rules, and the system disappears.

That is why Bitcoin is often compared to a protocol rather than a business. It is not trying to maximize revenue or growth in the same way a company does. It is trying to keep a rule set stable enough that users can trust it without trusting an issuer.

Proof of work and the cost of rewriting history

Bitcoin uses proof of work to make history expensive to rewrite. Miners bundle transactions into blocks and compete to add them to the chain. The process requires real-world energy, which helps secure the network against manipulation.

The result is not just a database. It is a ledger with economic weight behind it. In practice, that means rewriting the past becomes costly enough that the system can treat the current chain as reliable history.

♻️ Orange is the New Green : Understand how Bitcoin mining is influencing the energy industry

Why the 21 million cap matters

Bitcoin’s supply is capped at 21 million units. New coins are issued according to a schedule that becomes slower over time. That rule is not a marketing slogan. It is part of the protocol.

The important point is not only that Bitcoin is scarce. It is that the scarcity is auditable. Anyone can check whether the rules are being followed. That makes Bitcoin’s monetary policy radically different from fiat money, where supply decisions are delegated to institutions and can change through policy.

Keys matter more than accounts

Traditional money is someone else’s liability. A bank deposit is a claim on a bank. A fiat currency is supported by the state and the banking system around it. Bitcoin is different. It is not the debt of an institution.

That is why self-custody matters so much. If you control the keys, you control the bitcoin. If you do not, you are trusting someone else again.

For everyday payments, Bitcoin often relies on higher layers such as the Lightning Network. But the base layer remains the settlement system that defines ownership. That separation is important. Bitcoin does not need every payment to happen on-chain in order to matter. It needs the base layer to remain credible, because that is what gives the higher layers value.

Bitcoin vs Gold

Gold is the historical reference point people usually reach for when they talk about Bitcoin. That comparison is useful, but only if it is handled carefully.

Why gold became monetary

Gold became money because it had properties that made it useful as a store of value. It is scarce, durable, difficult to produce quickly, recognizable, and divisible to a degree. Those qualities made it a good candidate for savings and settlement long before modern banking existed.

Gold also had something else going for it: it was hard for rulers to create out of thin air. That is part of why it became a monetary benchmark in the first place. A scarce asset is not automatically money, but scarcity gives money credibility.

Why gold stopped working well in a modern economy

The problem is not that gold lost its value. The problem is that physical gold is awkward in a digital and global economy.

It is hard to move at scale. It is expensive to store safely. It is difficult to verify instantly. And once you want to use it in a modern payments system, you almost always end up relying on custodians, certificates, or claims on gold rather than the metal itself.

That is where the old problem returns: trust. Gold is scarce, but the modern user rarely touches the metal directly. The user touches a promise about the metal.

Bitcoin fixes the portability problem

Bitcoin takes the scarcity idea and makes it native to the internet. It is easier to transfer across borders. It is easier to store without a vault. It is easier to verify without a dealer. And it can be held directly, without needing a physical intermediary.

That is why Bitcoin is often described as “digital gold,” but the label is a little too small. Bitcoin is not just gold translated into software. It is a monetary asset with internet-native custody and verification.

But Bitcoin is not perfect gold yet

Bitcoin still has trade-offs. It is more volatile than gold. Its on-chain transactions are public. Its monetary history is short compared with gold’s. And it is still evolving as an asset and a network.

So the right comparison is not “Bitcoin is better than gold in every respect.” It is more precise than that: Bitcoin solves some of gold’s practical limits in the digital world, while introducing its own constraints.

Bitcoin vs Central Banks

If gold is the historical comparison, central banks are the institutional one.

Central banks were built for stability

Central banks exist to manage liquidity, support the banking system, act as lender of last resort, and influence the cost of credit. In theory, that helps reduce panic and keep the economy functioning.

In practice, it also gives a small group of institutions enormous influence over money, savings, and credit. That influence is not always visible day to day, which is precisely why it is easy to underestimate.

1971 changed the monetary order

The modern fiat era did not arrive overnight. It followed the slow collapse of the Bretton Woods framework, which tied major currencies to the dollar and, indirectly, to gold.

That system was still under strain for years, but 1971 is the symbolic break. That was the year official convertibility of the dollar into gold ended. From there, the monetary order moved fully toward fiat and flexible exchange rates.

Once that happened, money became even more political. The scarcity constraint that gold used to impose was gone, and the rules of the game became much easier to change.

What fiat money changes

A fiat system can be useful in crisis. It also makes it easier to lower borrowing costs, expand credit, support governments and banks, absorb shocks, and shift costs into the future.

But those benefits come with distortions. Cheap money can inflate asset prices. It can reward leverage. It can make saving in cash look irrational. It can widen the gap between people who already own assets and people who do not. The result is not simply “more money.” It is a different distribution of power across savers, borrowers, and asset owners.

Bitcoin replaces discretion with a rule

Bitcoin does not promise perfect policy. It does something simpler and, in a way, more radical: it replaces discretionary monetary management with a rule that is visible, stable, and difficult to change.

That rule is not “good” because a committee says it is. It is good, if it is good at all, because users can verify it for themselves. That is a very different model of money. It does not remove politics from society, but it does remove politics from monetary issuance.

The point is not that central banks are useless. The point is that Bitcoin offers a competing monetary logic, and that logic does not depend on trust in a committee.

💡 What will happen if Bitcoin fails to become a currency?

How Is Bitcoin Adopted Today?

Bitcoin is being adopted, but not always in the way its original design would suggest.

Most adoption still goes through intermediaries

A lot of users meet Bitcoin through exchanges, custodial apps, ETFs, treasury companies, brokers, and banks. That has helped Bitcoin reach a wider audience. It also means that many users still do not actually hold their own keys.

That is not always irrational. Self-custody has a learning curve, and mistakes can be expensive. For many people, a familiar intermediary is simply easier. If the first step into Bitcoin is an ETF or a custodial app, that is still a step into Bitcoin. The problem starts when the user never moves beyond that point.

The trade-off is obvious: the more Bitcoin is held by third parties, the more its users resemble the old financial system again.

Self-custody remains the core option

This is where Bitcoin remains different. Even if someone starts with an ETF or a custodial platform, the system still leaves open an exit path. A user can withdraw, hold keys directly, and stop relying on a third party. That option changes the balance of power.

It is easy to underestimate how important that is. Most financial systems make exit expensive or impossible. Bitcoin keeps exit as a real possibility. That possibility disciplines intermediaries, because it means the user is not locked in forever.

Adoption is not only about price

A lot of public discussion around Bitcoin focuses on the price. That matters, but it is not the whole story.

The deeper question is whether Bitcoin is being used as a speculative asset only, or whether people are actually learning to hold, verify, and move value without permission. If the answer is only “price exposure,” then Bitcoin has not yet become the monetary system it wants to be.

That is also where higher layers matter. A network like Lightning, or other payment tools built on top of Bitcoin, can make the asset more usable without changing the base layer. Adoption does not require every user to become a technical expert. It requires the stack around Bitcoin to become easier to use without taking ownership away from the user.

What Bitcoin Really Changes

Bitcoin’s most important innovation is not the price. It is the option it gives the user.

An exit from the old model

With Bitcoin, users can choose a different relationship to money. They can hold it directly. They can verify the rules themselves. They can move value without asking a bank for permission. They can store a scarce asset outside the balance sheet of a third party.

That is not a minor feature. It is the point. Most financial systems are built around delegation. Bitcoin gives the user a way to keep ownership close to the source of the value itself.

A monetary system with competition

Bitcoin also introduces competition into money itself. If fiat money depends on trust in institutions, Bitcoin gives users a way to opt out of that trust model. Not everyone will do it. Not everyone should. But the existence of the option matters, because it changes the background assumptions of the system.

That is why Bitcoin can matter even before it becomes a universal medium of exchange. A credible alternative can influence the behavior of the incumbent system. It does not have to replace everything to be relevant.

The real question is not whether Bitcoin exists

Bitcoin is already here. The question is what role it ends up playing.

Will it remain mostly a speculative asset held through intermediaries? Or will it gradually become a more direct monetary tool, one that people use to preserve value and transfer it without permission?

That outcome is still open. But the existence of the option is already changing the conversation around money, just as the existence of gold once did and just as the rise of fiat money once did in the opposite direction.

FAQ

Is Bitcoin better than gold?

Not in every respect. Gold is older and less volatile. Bitcoin is easier to move, easier to verify, and much better suited to the internet. They solve some of the same problems, but in different environments. The real comparison is not which one is “best,” but which one fits the world people actually live in now.

Can Bitcoin replace central banks?

Not directly. Bitcoin does not do monetary policy the way central banks do. What it can do is provide an alternative monetary system that does not rely on discretionary issuance. That alternative may remain smaller than the fiat system for a long time, but it still matters because it introduces a credible exit.

Is Bitcoin money or an asset?

It is both, depending on the context. People treat it as a store of value, a medium of exchange, and a speculative asset. Its monetary role is what makes it more than just another tradeable instrument. If you remove that monetary role, Bitcoin becomes much easier to misunderstand.

Why is Bitcoin limited to 21 million?

Because that rule is part of the protocol. The fixed supply is one of the main reasons Bitcoin is seen as scarce and predictable. It is also the reason people see it as fundamentally different from fiat money, where supply can be expanded through policy.

Is Bitcoin only used for speculation?

No. A lot of Bitcoin activity is speculative, but the system was designed for value transfer, settlement, and self-custody. Its long-term value depends on more than trading. The more Bitcoin is used as a monetary tool rather than only as a trade, the stronger that distinction becomes.

Conclusion

Bitcoin is not just a digital asset competing with other assets. It is a monetary system that tries to solve a deeper problem: how to preserve and transfer value in a world where money is increasingly digital, centralized, and mediated by third parties.

Gold failed to scale cleanly into that world. Central banks gave us stability, but also more discretion, more leverage, and more dependence on institutions. Bitcoin offers something else: a scarce digital currency that can be verified, held, and moved without asking permission.

That does not mean everyone will use it the same way, or that Bitcoin has already “won.” A lot of adoption still goes through exchanges, ETFs, and custodial products. But the more important question is whether users keep the option to exit that model.

That is where Bitcoin still looks different. Not because it has solved every problem, but because it has reopened a question that modern money had mostly closed: who should control the money, and how much of that control should be left to the user?

Sources and documentation: Bitcoin White Paper, Bitcoin transaction history, Bretton Woods system